UPS will be available as an option to the employees. Existing NPS / VRS with NPS as well as future employees will have an option of joining UPS. Choice, once exercised, will be final.

UPS will be available as an option to the employees. Existing NPS / VRS with NPS as well as future employees will have an option of joining UPS. Choice, once exercised, will be final.

The Unified Pension Scheme (UPS) introduces a significant option for government employees, both current and future, regarding their pension benefits. Here’s a detailed look:

-

Option for Existing Employees: Employees currently under the National Pension Scheme (NPS) or those who have taken Voluntary Retirement Scheme (VRS) with NPS benefits have the opportunity to opt for the UPS. This choice allows them to transition from the market-linked NPS to a scheme that promises a defined benefit.

-

Future Employees: New entrants into government service will also face this decision, choosing between the flexibility and potential higher returns of NPS or the security of a guaranteed pension under UPS.

-

Irrevocable Decision: Once an employee decides to join UPS, this choice is final. There’s no provision for switching back to NPS or any other pension scheme later, emphasizing the need for careful consideration before opting.

-

Assured Pension: Under UPS, employees are assured a pension equivalent to 50% of their average basic pay over the last 12 months before retirement, provided they have served for at least 25 years. For shorter service periods, the pension is proportionate but not less than after 10 years of service.

-

Family Pension: In case of the employee’s demise, their family will receive 60% of the pension the employee was entitled to, ensuring financial support continues for dependents.

-

Minimum Pension: There’s a minimum pension guarantee of ₹10,000 per month for those with at least 10 years of service, aiming to provide a basic level of financial security for all retirees.

-

Lump Sum Payment: At superannuation, in addition to the pension, employees receive a lump sum payment calculated at 1/10th of their monthly emoluments (pay + DA) for every completed six months of service, enhancing retirement benefits.

-

Inflation Indexation: The pension benefits under UPS are indexed for inflation, ensuring that the real value of the pension does not erode over time, which is a significant improvement over many existing pension schemes.

-

Implementation: The scheme is set to be implemented from April 1, 2025, giving employees time to understand and make an informed choice.

-

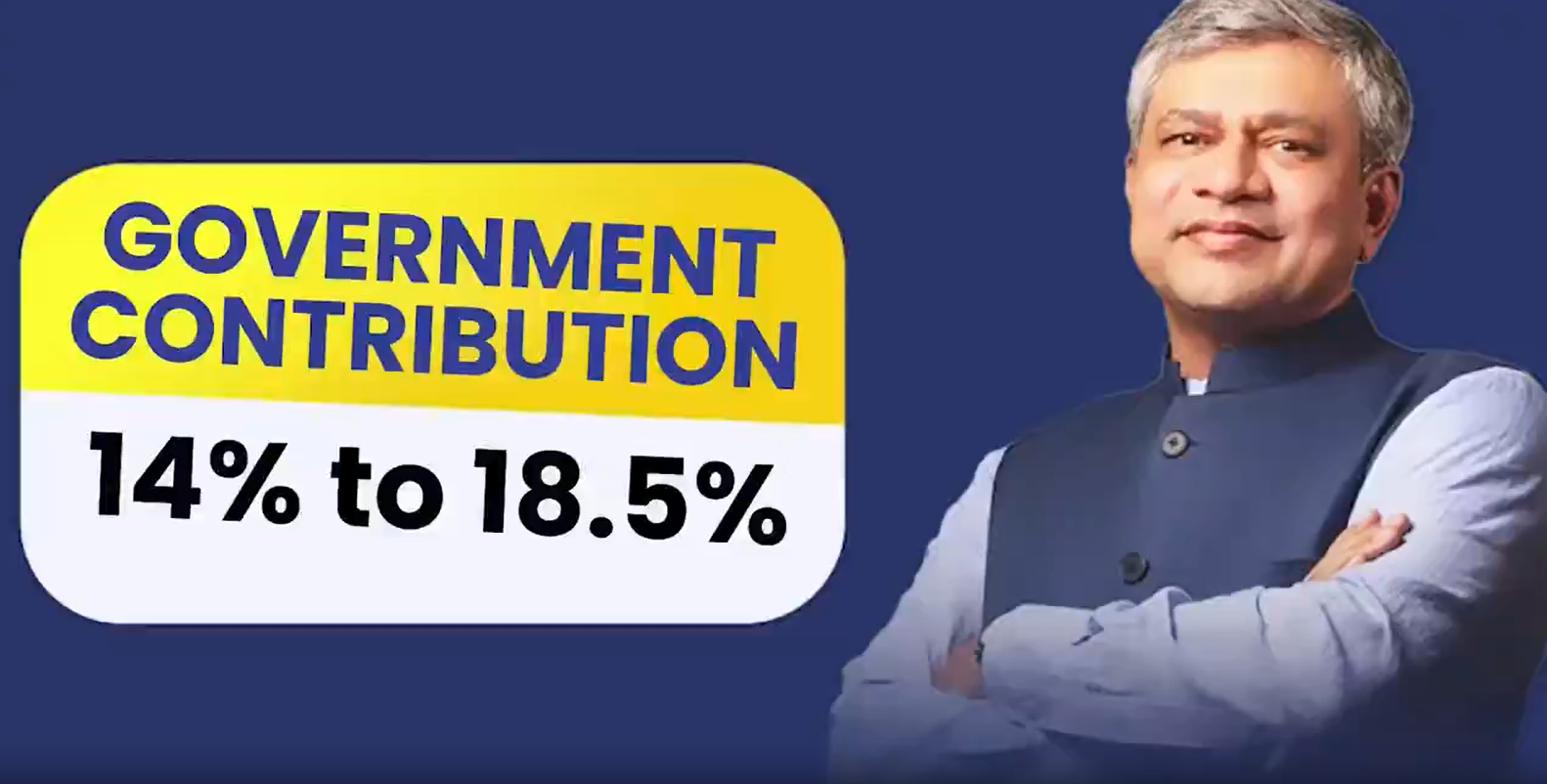

Contribution: While the UPS offers these benefits, it maintains the contributory nature of pension schemes, where both employee and government contribute, unlike the old pension scheme where the government bore the entire cost.

This scheme represents a hybrid model, blending elements of defined benefit and defined contribution pension systems, aiming to provide financial security while also managing fiscal responsibility for the government. Employees are encouraged to evaluate their financial needs, risk tolerance, and retirement planning before making this irrevocable choice between UPS and NPS.